The Fed Babble Bubble: What You Need To Know

One of the hallmarks of a speculative mania is that the bubble in question comes to dominate popular attention. If there’s one competitor to the never-ending fascination with the possibility of Trump presidency, it’s the unprecedented level of interest in the potential Federal Reserve rate hike.

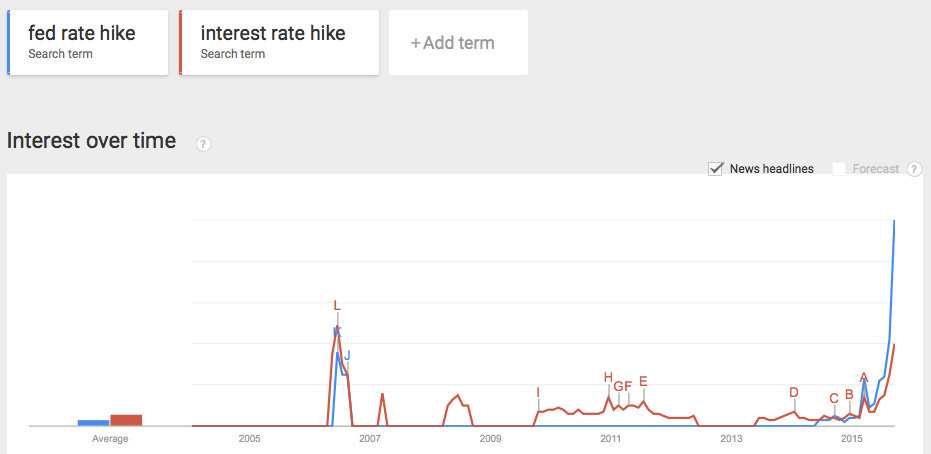

Consider this chart from Google Trends, which highlights the recent exponential increase in searches for "fed rate hike" and "interest rate hike."

You’re probably wondering: Why does everyone care? How can an interest rate set by the Federal Reserve affect you – and does it really matter if it rises by one quarter of one percent (0.25%)?

The blunt reality is that such a miniscule change won’t really matter. An increase of 25 basis points on a $250,000 mortgage raises the monthly payment by ~$34. For a $25,000 car loan, it’s about $3 per month--less than the cost of a lousy latte.

So what’s all the hubbub about? It can’t really be about the direct impact of rates on our lives, can it? Probably not. It’s really about the trend…because if the Fed begins to normalize the federal funds rate towards 3%, nobody will be safe from the economic ramifications.

The two biggest stones the Fed’s actions will likely throw into the global economic pond are higher credit costs and a stronger dollar. So what ripples will these produce? And how will they affect us?

First, if the Fed were to raise rates multiple times, the minor impact of higher credit costs I described earlier would not be so trivial. In addition to higher rates for credit cards and student loans, a 3% increase in the cost of a $250,000 mortgage would raise monthly payments by over $415 – about $20 per working day. Bye bye latte!

The ripples of the higher rate would also affect your investments. Do you have any bonds as part of your retirement savings? Well, when rates rise, bond prices fall. Equities may have already factored in the rate changes, but emerging markets may still be vulnerable. Your disappearing latte may also telegraph lower home prices. Bigger monthly payments means renting may be relatively cheaper, and there will be fewer buyers at given price levels.

Meaningfully higher credit costs also dampen economic activity. One estimate predicted a reduction of .15% in economic growth, and slower growth would mean around 30,000 fewer jobs created per month. Forget the raise you were hoping for…it’s probably not happening. Business investment spending would also fall. If you’d like to convince your boss you need an iPad Pro, hurry!

Second, the American dollar will likely appreciate against other currencies. So what? An appreciating dollar will dampen our export competitiveness, hurting industries from aerospace to pharmaceuticals. It also means US music and movies will be more expensive for foreigners to license.

Don’t expect to hear Katy Perry in the background of the latest Indian TV commercial.

But rising rates are not all bad news. Sure, the American economy will sour. Your portfolio may take some hits. You career prospects may suffer. And your industry may shrink in the face of serious headwinds. But as you drown any rate rise sorrows with retail therapy, you’ll be pleased to learn that imports from Chinese-made clothing to the Japanese-built Toyota Highlander will effectively be on sale. An appreciating dollar will also make overseas travel less expensive, so go ahead and plan that holiday escape to São Paulo or Paris.

Vikram Mansharamani is a Lecturer at Yale University in the Program on Ethics, Politics, & Economics. He is the author of BOOMBUSTOLOGY: Spotting Financial Bubbles Before They Burst (Wiley, 2011). Visit his website for more information or to subscribe to his mailing list. He can also be followed on Twitter.