Korean Market Collapse Forthcoming?

South Korea has the world's best performing stock market. Is it a bubble?

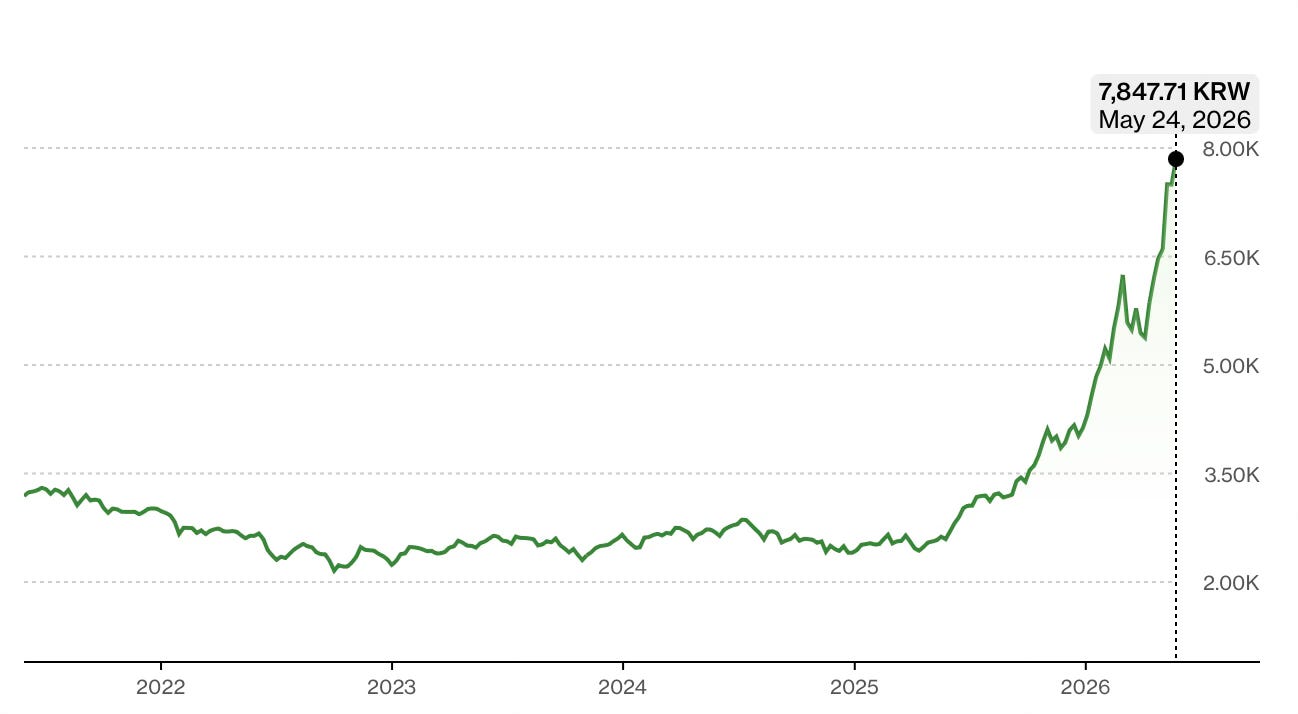

The South Korean stock market is booming. The KOSPI index is up about 150% from its April 2025 low and gained ~75% percent in 2025. This is Korea’s best performance in over 25 years. But it hasn’t stopped this year. It’s already up more than 75% and recently touched the 8,000 level for the first time in history. For comparison, it was hovering around 2,500 two years ago.

Regular readers know I’ve had a lifelong interest in bubbles. Unsurprisingly, performance like this catches my attention. Six days after hitting 8,000, the KOSPI plunged around 12%, triggering downside circuit breakers. The very next day it bounced 8% or so, triggering an upside circuit breaker. It was starting to look less like a rally and more like a seizure. My bubble spotting seismograph was indicating tremors afoot.

The dynamics get more concerning when you acknowledge that the meteoric rally has been largely fueled by the performance of two stocks: Samsung Electronics and SK Hynix. Both make the high-bandwidth memory chips that power Nvidia’s AI accelerators, and as the media put it bluntly: “Without Samsung and Hynix, there would be no KOSPI at 6,000” (not to mention 8,000).

So, the question I ask myself is simple: Is this a bubble?

My 2011 book on bubbles provided a framework for thinking about how to answer this question. The book was based upon a class I taught at Yale, and offered a multi-lens approach to spotting bubbles before they burst. I suggested the use of five lenses (microeconomics, macroeconomics, psychology, politics, and biology) to explore and evaluate sustainability of a boom. At root, it was based on my belief that every perspective is limited, biased, and incomplete…so why not use more than one?

So, let’s run the KOSPI through my framework.

Microeconomics Lens = Bubbly

Traditional economics suggests that when prices rise, demand is depressed and supply is motivated. But what if the opposite happens? What if higher prices lead to more demand? Might a self-fulfilling dynamic of higher prices leading to higher demand lead to even higher prices (and even higher demand)?

The KOSPI is a capitalization weighted index, meaning that the large companies exert more influence on the index. It also means that as heavyweights like Samsung rise in value faster than other components, their weight in the index rises. Continued positive performance compounds this dynamic, leading to a narrowing of breadth and a limited set of companies that drive the index performance. Today, Hynix and Samsung are about 50% of the index…and their earnings depend on a bet that AI infrastructure keeps booming. KB Securities calls this “a textbook feature of a late-stage bubble”: narrowing leadership, concentration in a few names, retail money piling in behind them. It’s what happened with the Nifty Fifty in 1971 and the dotcom stocks in 1999.

Macroeconomics Lens = Bubbly

When investors can easily borrow money to invest, my alarm bells go off because this too can create a bubbly dynamic. And through this lens, Korea looks vulnerable. Margin loan balances hit a record $27 billion on May 15, the very same day the KOSPI touched 8,000. And because the margin interest rates are hovering in the 7%-9% range, this implies retail investors are convinced the index will do better.

Credit magnifies both the upside and the downside. Think of it as a two-edged sword, and slight changes in credit can turn a virtuous upside cycle into a vicious downside one. Consider the story of a Korean civil servant who put 2.3 billion won ($1.7 million) into Hynix, most of it borrowed. Might that end badly? When the KOSPI dropped 12 percent, forced liquidations surged to 6.5 percent of unsettled trades and $625 billion in market value vanished in a single session.

Psychology Lens = Bubbly

Anyone who studies financial bubbles understands that investors swing between greed and fear. Times with widespread and extreme investor fear are usually good times to buy. The flip side is that widespread and extreme investor greed is a good time to sell. And while data such as foreign investor selling may dampen bubble concerns, Korean retail investors are suffering from stratospheric levels of FOMO (fear of missing out). They’ve absorbed more than $13.2 billion of foreign investor selling last week alone and are doing so with margin debt.

{kind=link}

Investor overconfidence is a tell-tale sign of bubbly conditions and record Korean margin debt and buying in the face of intense selling from foreigners seems to be pointing to a bubbly KOSPI. ZeroHedge recently called Korean retail investors “levered to the gills and out of funds, buying with the bank’s money.” South Koreans are even cashing out insurance policies to play the market, eerily reminiscent of the ordinary people flooding the market for tulip bulbs in 1637, with some even mortgaging their homes. When the smart money exits and the crowd doubles down on borrowed cash, it’s starting to look as bubbly as a glass of champagne.

Political Lens = Sort of Bubbly.

Government actions often also play role in fueling bubbles. This was true in the great financial crisis as government policies created moral hazard in the mortgage market, allowing a social objective of greater homeownership to create and reinforce risky lending. Political leaders thinking about market performance as a report card for their political acumen is also a concerning dynamic.

South Korean President Lee Jae Myung vowed to hit KOSPI 5,000 and his “Corporate Value-up Program 2.0” mandated governance reforms, strengthened shareholder protections, and slashed dividend income tax in half to 25%. These are real, structural improvements. But when a government explicitly targets a stock index number, it creates a political incentive to keep the party going—and a political cost to letting it correct.

Biology Lens = Bubbly.

In the past, I’ve often described a bubble as an infection that spreads rapidly across a society, eventually reaching epidemic breadth before “herd immunity” leads to a correction. The AI narrative is a great case in point, and it’s jumped from Silicon Valley to Seoul in less than two years. Samsung’s HBM4 chips, SK Hynix’s Nvidia contracts, and the “semiconductor supercycle” are all mechanisms to spread the AI virus to more and more people. The Korea Times identified it as a “gray rhino”: plainly visible, widely recognized, and frequently underestimated. The number of people without any exposure to the artificial intelligence story is dwindling rapidly.

AI Infrastructure: Boom or Bust?

In the late 1990s, Lucent Technologies was America’s most widely held stock — a “picks and shovels” play on the internet revolution. The company lent billions to its own customers so they could buy more Lucent equipment. On paper, revenue soared. In reality, Lucent was financing its own demand. When the customers went bust, Lucent nearly followed. The p…

Epidemics don’t end because the virus weakens. They end when everyone susceptible has already been infected. And with the case of Artificial Intelligence, herd immunity is nigh. In markets, that means the rally ends when everyone who’s going to buy has already bought—on margin, at the top. There are no more greater fools left to join the party. When taxicab drivers and bellman start talking about the market, the bubble is close to bursting.

So where does this leave us?

My assessment is that the Korean markets are very bubbly and unsustainable. Record margin debt, forced liquidations, and professional investors selling while retail investors sell life insurance to buy the market are big bright flashing warning signs. And the fact that everyone, and I mean everyone everywhere, is talking about AI adds a level of caution to anything dependent upon that story continuing.

I’ve often said that investors are destined to make mistakes. None of us is perfect. But we do have a choice in the type of mistake to make. There are errors of commission in which investors own a bubble that eventually leads to losses. And there are errors of omission in which investors miss the final stages of a bubble and miss gains.

Korea is not a market I’d chase. Yes the AI semiconductor story is real and Samsung and Hynix are world-class companies that will benefit from the global transformation underway. But a good story and a good investment are not the same thing, especially when leverage is maxed out, the institutions are heading for the exits, and the government is promising the party won’t end. Now’s the time to make errors of omission…

VIKRAM MANSHARAMANI is an entrepreneur, consultant, scholar, neighbor, husband, father, volunteer, and professional generalist who thinks in multiple-dimensions and looks beyond the short-term. Self-taught to think around corners and connect original dots, he spends his time speaking with global leaders in business, government, academia, and journalism. He’s currently the Chairman and CEO of Goodwell Foods, a manufacturer of private label frozen pizza. LinkedIn has twice listed him as its #1 Top Voice in Money & Finance, and Worthprofiled him as one of the 100 Most Powerful People in Global Finance. Vikram earned a PhD From MIT, has taught at Yale and Harvard, and is the author of three books, The Making of a Generalist: An Independent Thinker Finds Unconventional Success in an Uncertain World, Think for Yourself: Restoring Common Sense in an Age of Experts and Artificial Intelligence and Boombustology: Spotting Financial Bubbles Before They Burst. Vikram lives in Lincoln, New Hampshire with his wife and two children, where they can usually be found hiking or skiing.